Introduction

Professional service contracts traditionally rely upon relatively familiar commercial mechanisms: agreed hourly charge-out rates, named staff grades, schedules of time charge rates with annual uplifts for inflation. The NEC3 Professional Services Contract broadly reflected that position. Under the cost reimbursable options, the contract was operated by reference to the staff rates for time charge stated by the Consultant in the contract data.

The NEC4 edition of the Professional Service Contract (PSC4) takes a very different approach. Rather than relying on agreed commercial charge-out rates, the cost reimbursable Options C and E adopt a payment methodology similar to that used in the other long-form versions of the NEC4 contracts. The payment regime is based on the rules governing Defined Cost and fixed percentages for overheads, risk and profit.

In a three-part series of articles, I will look at the PSC4 payment regime, explaining in detail why the recoverable cost is no longer driven primarily by what a consultant ordinarily charges in the market, but by what the contract permits to be recovered. In part one, I examine the foundations of that regime, focusing on the defined cost of people.

Main difference between Option A and the cost reimbursable Options C/E

Main Option A is fundamentally a priced contract with the rules governing Defined Cost applicable only for compensation events. When assessing cost for compensation events under Option A, agreed People Rates stated in the Contract Data are used. Under main Options C and E, a more detailed cost recovery methodology is applied, built around Defined Cost.

Defined Cost under Main Options C and E

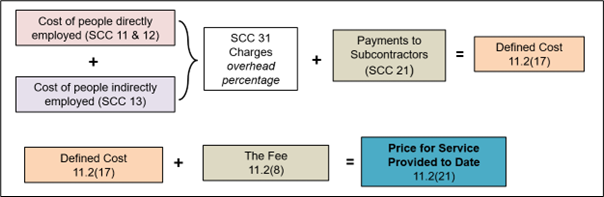

Main Options C and E are cost-based contracts. The Consultant is not paid its actual cost incurred, with recoverability depending on whether the cost falls within the contractual definitions, plus a fee. This payment regime is reflected in the definition of the Price for Service Provided to Date under clause 11.2(21). Clause 11.2(8) defines the Fee as the amount obtained by applying the fee percentage to the Defined Cost.

The rules of Defined Cost setting out what is recoverable are given in clause 11.2(17), which states:

‘Defined Cost is the cost of the components in the Schedule of Cost Components less Disallowed Cost.’

Clause 52.1 then establishes an important commercial principle:

‘All the Consultant’s costs which are not included within Defined Cost are treated as included within the Fee.’

Figure 1 (below) provides a simplified model of the PSC4 payment regime examined in this series of articles. The following sections consider each element of that model in more detail, beginning with People costs.

Figure 1: Defined Cost plus the Fee using the Schedule of Cost Components

Schedule of Cost Components

The Schedule of Cost Components, sometimes colloquially referred to as the ‘long schedule’, consists of four main components:

1 People (items 11, 12 & 13)

2 Subcontractors (item 21)

3 Charges (item 31)

4 Insurance

People cost component items 11, 12 & 13

Cost component 11 deals with payments made to the person directly employed by the Consultant (salary), and payments made in relation to that person, e.g. employer’s national insurance contributions, pension and company cars. Cost component 12 provides an additional list of items paid to or in relation to the person in accordance with their contract of employment, including bonuses, overtime, protective clothing and safety training.

The cost components for people are strictly limited to those that are ‘providing the service’, with support people and office overheads being covered separately in the overhead charge component 31 (see below).

The first paragraph of cost component 11 states that (defined) cost is:

‘calculated by dividing the total of the following payments by the total time recorded

with the resulting amount multiplied by the time recorded for work on the contract.’

This makes it clear that payment relies on using a time-based method, although the contract does not make an express reference to hourly rates or time charges. In practice, the methodology commonly results in an average annualised cost-based hourly rate.

The total time recorded on the Consultant's time recording system will depend on the person's contract of employment and what time the recording system is designed to capture. Typically, for a person employed full-time, the total number of hours will range from 1900 to 2000 hours in many UK consultancies. On one interpretation, and depending upon how the Consultant’s time recording system operates, total time may include bank/public holidays, annual leave and all other non-fee earning time. e.g. training, general administration tasks and medical appointments. Over time, if booked, would be additional.

The total of the payments made to and in relation to the person (cost components 11 & 12) will also depend on the person's contract of employment. A significant proportion of the cost will be salary, but as can be seen from the list of other items in the Schedule of Cost Components, salary is not the only cost. Typically, these additional costs are between 30 to 60% of base salary. Although the contract does not use multipliers to assess the Defined Cost for people, a useful indicator of the hourly “cost” rate for a person earning an annual salary of £60,000 could be calculated as follows:

The hourly rate calculated above is clearly significantly less than a typical ‘selling rate’ for that person. The reason is that it excludes costs associated with the Consultant's support people and office overheads (cost component 31) and the Fee. An explanation of the overhead charge and fee percentage is given in parts 2 and 3 of this series of articles.

For people who are indirectly employed (cost component 13), the Defined Cost is the amounts paid by the Consultant according to the time properly spent on work in the contract. This is relatively straightforward, but a distinction may need to be made between people who are genuinely employed as agency staff and those who qualify as Subcontractors as defined in clause 11.2(14). Here, it is important to note that costs associated with indirectly employed people under the cost component 13 are subject to an additional overhead charge (SCC 31) whilst Subcontractors are not.

The People cost components represent only the first stage of the PSC4 payment build-up. The interaction between SCC11-13, SCC31 Charges, Defined Cost, the Fee and Disallowed Cost is illustrated in the diagram included in part 2 of this series of articles.

Conclusion

The PSC4 cost reimbursable payment regime represents a clear departure from traditional consultancy charging models and its NEC3 predecessor. Under Options C and E, recoverability is built around Defined Cost and contractual cost rules rather than agreed commercial charge-out rates. The treatment of people cost sits at the centre of that approach.

The Schedule of Cost Components 11, 12 and 13 establish a methodology based upon actual employment-related cost, time recording and contractual categorisation. The resulting figures may bear limited resemblance to conventional consultancy selling rates, but that is largely because the PSC4 methodology deliberately separates direct people cost from the wider cost of supporting and operating the business.

In part 2 of this series, I examine Subcontractors, the overhead percentage and the Fee.

David Hunter

May 2026