In part 1 of this series, I examined the basis of the payment regime under Options C and E of the NEC4 Professional Service Contract (PSC4), focusing on Defined Cost and the treatment of people costs. I explained how the PSC4 departs from traditional consultancy charging models by adopting a regime built around Defined Cost rather than agreed commercial charge-out rates.

A key conclusion from Part 1 was that the People cost components in the Schedule of Cost Components (“SCC”) do not represent a conventional consultancy selling rate. Instead, they form only the first layer of the PSC4 cost build-up. This second article develops that analysis by considering Subcontractors, the overhead percentage under SCC 31 and the Fee. In doing so, it examines how the contract bridges the gap between people costs, business overheads, corporate risk and profit.

Subcontractors cost component 21

Cost Component 21 covers payments to Subcontractors. The term ‘subcontractor’ may not be synonymous with professional service contracts. In fact, the NEC3 Professional Services Contract uses the term ‘Subconsultant’. However, with the objective of consistency, all the NEC4 forms of contract use the term ‘Subcontractor’. Clause 11.2(14) of the PSC4 defines a Subcontractor as:

‘ a person or organisation who has a contract with the Consultant to provide part of the service, except for the supply of people paid for by the Consultant according to the time they work.’

The definition appears to differentiate between a true subcontractor and agency staff or sole traders, the latter of which are intended to be covered under cost component 13. As noted previously, the overhead charge derived from cost component 31 is not applied to the cost of Subcontractors. A Consultant wishing to include risk and earn a profit from subcontracted work would need to make such allowances within its fee percentage.

Charges cost component 31 – the overhead percentage

Cost component 31 of the Schedule of Cost Components introduces the overhead percentage. It states:

‘A charge for support people and office overhead costs calculated by applying the overhead percentage stated in the Contract Data to the total of people items 11, 12 and 13. The charge includes provision and use of people, accommodation, equipment, supplies and services required to provide the office and to support people providing the service.’

Cost component 31 does not attempt to produce an exhaustive or detailed list of what costs are included in the overhead charge. That is perhaps sensible approach given that consultancy businesses vary significantly in size, structure and operating models. Nevertheless, in practical terms, it is conceivable that the overhead percentage could cover the following costs:

- Non-fee-earning Directors and Managers

- Accounts/finance/payroll team

- Purchasing department

- HR personnel

- Health, Safety and Welfare functions

- Quality assurance and governance

- Accommodation costs: – office rent, cleaning & maintenance, security, buildings insurance

- IT support

- IT equipment, software licences

- General office supplies

- Administration and general business support activities.

The overhead percentage performs an important commercial role, bridging some of the gap in operating costs that are not part of the defined cost for people covered by SCC 11, 12 & 13). It recognises that the cost of providing services is not limited to the cost of employing those who are directly performing work for the contract.

Modelling work by Daniel Contract Management Services has shown that typically, an overhead percentage of between 30 and 40% could reflect the true coverage of overhead costs under the PSC4 cost reimbursable payment regime. In a recent survey carried out by Daniel Contract Management Services, 9 out of 10 people said they most commonly saw the overhead percentage less than 25%. The results indicate that the industry may not fully understand how the PSC4 is intended to operate. Alternatively, respondents to the survey could be working under contracts where the rules on Defined Cost have been amended to reflect a more traditional time charge regime. Otherwise, it would seem that Consultants providing services under the cost reimbursable options are not recovering all of their overheads.

Charges for support people and office overheads are listed under cost component 31 and therefore fall under the definition of Defined Cost as stated in clause 11.2(17). However, as the amount of charge is calculated from applying the overhead percentage to the people cost, it is not itself readily identifiable as a discrete payment made by the Consultant. It therefore seems doubtful that the overhead percentage (stated in Contract Data) nor the charge amount forms part of the ‘accounts of payments of Defined Cost’ the Consultant is obliged to keep records of under clause 52.3 (bullet point 1). The overhead percentage charge and the charge amount would therefore not appear to be part of the 'accounts and records' which are subject to the Service Manager’s inspections under clause 52.4 and consequently, not capable of forming part of Disallowed Cost under the first bullet clause 11.2(18). This position is probably what the NEC contract drafters intended.[i] Consultants should, however, remain aware of contract amendments made by the Client that may alter this position.

The Fee – Clause 11.2(8)

Clause 11.2(8) defines the fee simply as:

‘..the amount calculated by applying the fee percentage to the amount of Defined Cost.'

A Consultant approaching the PSC4 using conventional commercial instincts might be tempted to view the Fee simply as profit and corporate overhead. However, the extent to which allowances should be made for the Fee cannot be properly considered without taking account of the effects of clause 52.1, which states:

‘All the Consultant’s costs which are not included in the Defined Cost are treated as included in the Fee.’

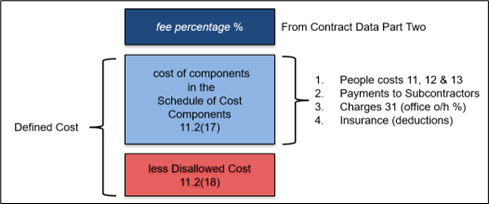

As a reminder, Defined Cost is all those costs covered by the Schedule of Cost Components, including the overhead charge, less Disallowed Cost. However, the rules governing what is recoverable by the Consultant as Defined cost do not cover all costs.

The PSC4 payment regime can be easier to understand when viewed as a structured commercial build-up. Figure 2 below illustrates the interaction between People costs, the SCC31 overhead percentage, Defined Cost, the Fee and the subsequent effect of Disallowed Cost.

Figure 2: Schedule of cost components less Disallowed Cost, plus the Fee

What exactly still needs to be recovered through the Fee?

To what extent costs not captured by Defined Cost need to be allowed for in the Fee will vary between businesses. Below is a checklist of typical cost items, including profit, that should be considered when building up the fee percentage.

- Legal costs

- Professional Indemnity insurance

- Employer’s liability insurance

- Public liability insurance

- Other insurances e.g. legal costs insurance, business continuity, etc.

- Training and development

- Professional membership fees

- Safety training for non-fee-earning staff

- Staff expenses incurred NOT providing the service

- Cost of non-fee-earning time for people who would otherwise be providing the service, including utilisation and efficiency

- Risk of disallowed cost

- Allowance for risk of costs included in the fee

- Allowance for cash flow risk due to the delayed payment of insurable events

- Profit on the defined cost work that is performed by subcontractors

- Profit on the defined cost of work that is performed by people directly and indirectly by the Consultant

The fee percentage will depend on how a business is structured, its corporate governance and approach to risk and profit. However, given the wide coverage of what is deemed to be included in the fee for a true assessment, it should not be a surprise to see fee percentages ranging between 30 and 40%. In a recent survey carried out by Daniel Contract Management Services, 6 out of 10 people said they most commonly saw the fee percentage between 10 and 20%. Less than one in ten people said the fee percentage was above 30%. These survey results again call into question how the PSC4 is being operated and to what extent the payment regime is understood.

Conclusion

PSC4 Options C and E adopt a layered approach to recoverable cost that differs materially from traditional consultancy charging models. The overhead percentage (Charges) and the percentage fee cover different costs and are applied separately.

The overhead percentage is applied to People cost components in SCC 11, 12 and 13. The Fee then performs a further commercial function, absorbing costs, risks and allowances not captured elsewhere within Defined Cost. In Part 3 of this series, I examine two further aspects of the PSC4 payment regime that are often misunderstood but commercially significant: Insurance and Disallowed Cost.

David Hunter

May 2026 (revised Aug 2026)

[i] The author acknowledges contributions made by Richard Patterson of Mott MacDonald on this aspect of Defined Cost.